The Egyptian Minister of Petroleum and Mineral Resources visited Palestine and Israel on 21 February to bolster the objectives of the East Mediterranean Gas Forum. During the visit, the Egyptian and Israeli governments approved an agreement between Egyptian and Israeli companies to extend a new marine gas pipeline to connect the Israeli fields, Tamar and Leviathan, with the East Mediterranean gas line, which was established with the purpose of transporting Egyptian gas to Israel. This line is different than East-med, which was planned to connect Israel, Cyprus, Greece and Europe during former president Hosni Mubarak’s rule.

Similarly, the Egyptian and Palestinian parties signed a memorandum of understanding between the partner parties in the Gaza field to develop it with Egyptian expertise, while benefiting from Egypt’s experience. This step comes within the framework of strengthening Egypt’s position as a regional hub for energy circulation. This article is meant to provide insight into the Egyptian visit, its timing, and its connection to Israel’s efforts to increase its ability to export gas, while serving the Egyptian goals.

The context

Israel discovered the Tamar gas field during the first decade of the century with a total of 280 billion cubic meters (m3) of gas reserves. This was followed by the discovery of the Leviathan field in 2010 with a total of 620 billion m3 of reserves, then Cyprus joined it with the Aphrodite field in 2011, with 200 m3 of reserves. In the beginning, both countries depended on exporting to the Egyptian market, which had been suffering from a decrease in the domestic production of gas since 2014, creating plans to exploit these huge reserves. However, Egypt discovered the Zohr gas field in 2014 with 850 m3 of reserves, so the country became able to achieve self-sufficiency in the foreseeable future, which already happened by September 2018. At the same time, the Israeli gas was employed for local use and exported to Jordan, as shown in the following table:

Table 1- Domestic consumption and Israeli export agreements in 2019

As indicated above, the Israeli domestic consumption doesn’t exceed one percent of the reserves, while the total quantities agreed to be exported to Jordan are about 5.3 percent of the total reserve; meaning that larger quantities must be exported in order to be able to adequately benefit from the massive reserves. All this requires the existence of a huge market that can accommodate both the Israeli and Cypriot supplies. Similarly, an export platform is needed, whether its pipes connect to the market or liquefaction stations to send it via the sea, which is what both countries worked on since they signed a memorandum of understanding with Greece, the European Union and the United States, with the purpose of establishing a pipeline linking them to Europe. Its construction was scheduled to be completed in 2025, with the possibility of the quantity transported reaching 15 billion m3.

As a result, Israel and Cyprus had no other option in the foreseeable future except to exploit the Egyptian liquefaction terminals for export to Europe, and in light of the political problems of connecting Turkey via Cyprus using a marine gas line, the countries were prompted to sign two re-export agreements, after the liquefaction of the two Egyptian facilities. This constituted an incentive for the tripartite, Jordan, Greece and Italy, to form an international organization with the purpose of facilitating the circulation of gas, which resulted in the signing of the Charter of the East Mediterranean Gas Forum Organization, on 23 September 2020, to enhance cooperation between the exporting countries and the countries on the route to Europe. The previous steps all served the Egyptian efforts to transform itself into a regional hub for the export of gas to Europe. Achieving this became dependent on three determinants; agreements to export gas from the producers in the basin; pipelines to transport gas to the liquefaction facilities; and the carrying capacity of the liquefaction facilities themselves, which are reviewed in detail as follows:

Egypt-Israel gas agreements

On 19 February 2018, the Israeli Delek Drilling and its American partner Noble Energy signed two binding agreements with the Dolphinus Holding company, agreeing that the latter would import gas then supply it to the Egyptian liquefaction facilities with the purpose of liquidating it and re-exporting it to Europe. Moreover, the agreed upon quantity to export reached 64 m3 from the Tamar and Leviathan fields over 10 years, in an agreement worth $15 billion, binding from 2020 to 2030.

On 3 October 2019, the three involved companies agreed to amend the previous agreement, with the aim of increasing the quantities exported to Egypt by 34 percent to reach 85.3 m3 in 2035. This way, the agreement’s worth increased from $15 billion to $19.5 billion, and increasing exports from the Leviathan field to 60 m3, and decreasing the quantities from the Tamar field from 32 m3 to 25.3 m3. On 15 January 2020, the first imported shipment arrived to Israel with the quantities reaching 1.5-3 billion m3 annually during 2020, then rising in 2021 to 4-5 billion m3, then reaching about 7 billion m3in 2022.

Egypt’s liquefaction facilities

- Egypt has two liquefied natural gas facilities, Idku and Damietta.

- Idku facility

- It’s the largest in Egypt, including two natural gas liquefaction units with a capacity of 4,551 m3 per year of gas per unit, with a total of 9.1 m3 per year.

- The factory is jointly owned by the General Petroleum Corporation (12 percent), EGAS (12 percent), Shell (35.5 percent), Malaysia’s Petronas (35.5 percent) and the French ENGIE (five percent).

- The facility’s first operation was in 2005 and it operated during the fiscal year 2018/2019 as well, exporting about 4.89 m3 annually through 45 liquefied gas cargoes.

- This means the Idku facility has already exported around half its capacity, even before the arrival of the Israeli-Cypriot gas or the Zohr field’s production at its peak.

- By the end of 2020, the facility reached its production peak at about eight million tons per year

- Consequently, Egypt’s plan to become the regional hub for gas handling has become in dire need of the Damietta facility, so that the Egyptian export capacity can rise to 13.32 m3 per year, enabling the country to continue receiving the Israeli-Cypriot gas.

- The Damietta facility

It consists of one liquefaction unit and its production capacity is about 5.55 m3 per year. The facility began production in 2004, yet stopped working for eight years due to a legal dispute between the partners, the most important of which are the Spanish Nature Fenosa and the Egyptian government. After the latter filed arbitration cases, the Egyptian ability was expected to be reduced by 35 percent. From here, the Israeli gas companies started searching for alternatives to the suspended factory, the most important of which was building a floating liquefaction facility between the two Israeli fields, which would contribute to increasing the exports.

At the same time, the aforementioned cases ended with a ruling to fine the Egyptian government $2 billion, to compensate for the Egyptian authority’s halt in supplying the facility with gas in 2012, following the decline in domestic gas products. Nevertheless, Egypt didn’t pay that sum, instead engaging in talks with the company to settle the dispute with the mediation of Italy’s Eni, whose success was already announced on 2 December 2020. The agreement stipulated the exit of Naturgy, while distributing its shares among Eni, EGAS and the General Petroleum Corporation. The ownership structure was as follows: 50 percent for Eni, 40 percent for EGAS and 10 percent for the General Petroleum Corporation. Resultantly, the facility returned to work by loading two shipments, on 21 February 2020, of LNS from Damietta Port, one of them with a volume of 0.06 million m3. As a result, the Egyptian capabilities increased to 13.32 million m3 per year, at the present time and is ready to receive more Israeli and Cypriot gas. It remains in the hand of Egypt and Israel to raise the efficiency of the gas pipelines that connect the Israeli-Cypriot fields with the Egyptian facilities.

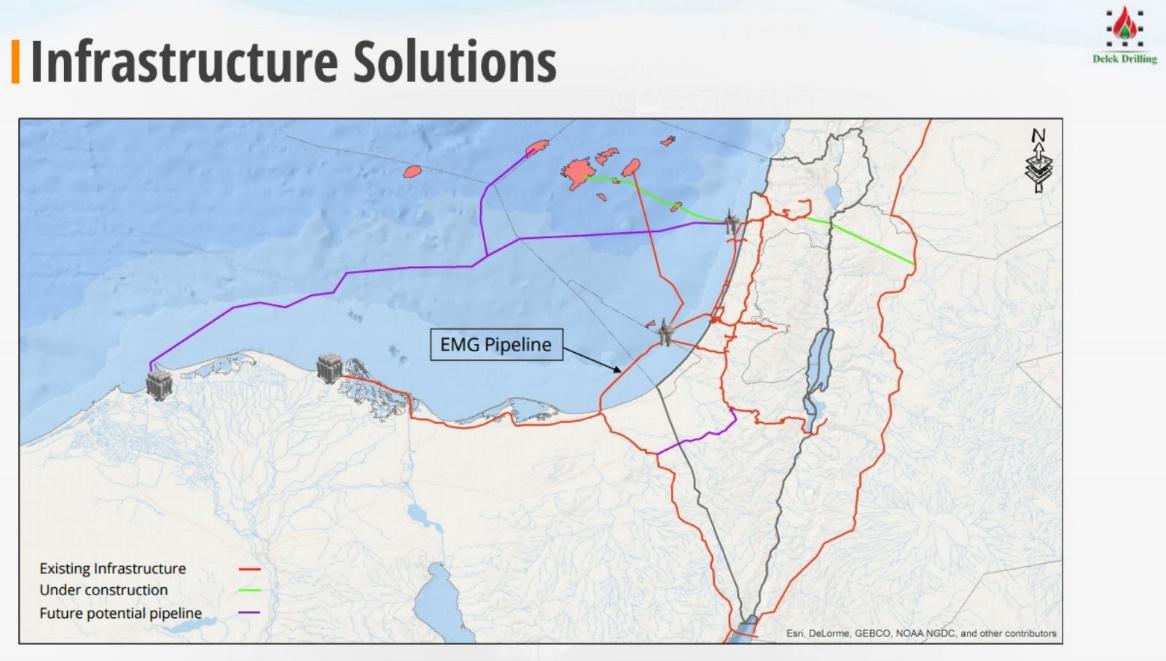

Egypt’s gas pipelines

Egypt is mainly linked to Israel via the Eastern Mediterranean Gas Pipeline, used to carry Egyptian gas to the Israeli Electricity Company which was considered insufficient to accommodate the huge quantities of gas agreed to be transported to Egypt for liquefaction. So it was first developed, before the agreement to establish a gas pipeline during the Minister of Petroleum’s recent visit to Israel.

1- The Eastern Mediterranean pipeline

- A pipeline to transport Egypt’s natural gas from Al-Arish, Egypt, to Ashkelon, Israel, which was within the Egyptian and Israeli territorial waters of the Mediterranean, extended for 100km. It was previously owned by the Egyptian Eastern Mediterranean Gas Company.

- The pipeline was purchased by a group of Israeli companies and the shares were distributed as follows: Delek (25 percent), Noble (25 percent) and East Gas (50 percent). In January, the rehabilitation process ended at a cost of 27 million shekels, in order to raise its efficiency and increase the quantities pumped into it.

- The duplication of the Eastern Mediterranean pipeline

- On 19 January, the partners of the Leviathan and Tamar fields announced an agreement where the Israeli Natural Gas Lines Limited (INGL) would extend a new subsea pipeline parallel to the first one.

- The new pipeline will cost $228 million and the expansion work will pay the Israeli companies 56 percent of the new pipeline.

- The Egypt-Cypriot pipeline

- In September 2020, Egypt held intensive talks with Cyprus with the goal of establishing a new direct marine natural gas pipeline, with the cost of $1 billion to connect the two countries, while linking the Cyprus Aphrodite fields with liquefaction stations in Egypt before re-exporting it.

- According to an agreement ratified by the president in July 2019 to establish the pipeline in September 2018, the Egyptian government is expected to receive Cypriot gas in 2022.

In sum:

- The Egyptian plans to transform into a regional center for energy trading is linked to three factors: agreements to buy gas from Israel and Cyprus; the capabilities of the Egyptian liquefaction facilities; and gas pipelines from the Israeli and Cypriot fields to these facilities.

- By the end of 2020, Egypt had operated the liquefaction facility in Idku to its full capacity, before the capacity to receiving all exports from Israel as included in the agreements was completed.

- Egypt worked on ending the legal dispute over the Damietta facility to raise the capabilities to the maximum, and the two agreements will continue to be implemented.

- Accordingly, Israeli companies first agreed to develop the existing gas pipeline followed by building a new gas pipeline until it absorbs the agreed quantities by 2022.

- The agreement and the Petroleum and Mineral Resources Minister’s visit to Israel were of utmost importance for the Egyptian project aimed at transforming Egypt into a regional energy hub.