The World Bank has released its latest report on world development entitled “World Development Report 2022: Finance for an Equitable Recovery”, which looks into the central role of financing in the economic recovery from the Covid-19 pandemic which gave rise to the greatest economic crisis the world has witnessed in over a century.

In 2020, about 90 percent of countries recorded a contraction in economic activity by about three percent, the global poverty rate soared, and governments adopted policies that would mitigate the economic consequences of the pandemic. However, governments’ responses brought about several economic vulnerabilities. The development report sheds light on four of the pressing risks arising from the pandemic, including the mounting non-performing loans, the delayed settlement of critical loans, credit crunch, and higher sovereign debt.

I- Covid-19 and Emerging Economic Risks to Recovery

The Covid-19 pandemic has had knock-on effects on all economies, which prompted governments to launch economic programs that have proved effective in the short term. Nevertheless, this emergency response by governments gave rise to new risks, including the public and private over-indebtedness and a global rise in poverty and inequality rates, with greater income losses among youth, women, and the self-employed and seasonal employment of low-educated workers. Women were particularly affected by the loss of income and employment because they were more likely to be employed in sectors that were more affected by lockdown and social distancing measures.

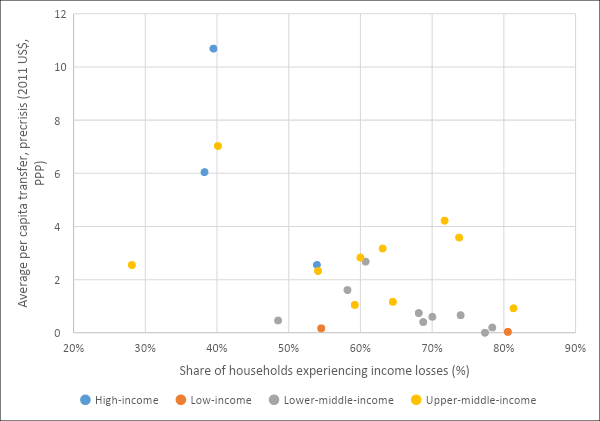

Data indicates that more than 50 percent of households in emerging and advanced economies have not been able to sustain basic consumption for more than three months in the event of income losses. Figure 1 shows income losses during the pandemic by country income group.

Figure 1: Loss of income by country income group

Similar patterns of income loss exist among businesses. Smaller businesses, informal businesses, and businesses with limited access to the formal credit market have been severely affected by income losses caused by the pandemic. Larger firms, though, have weathered the crisis as they had the ability to cover their expenses for up to 65 days, compared to 59, 53, and 50 days for medium-sized, small, microenterprises businesses, respectively.

II- Covid-19 and Risks Facing Bank Balance Sheets

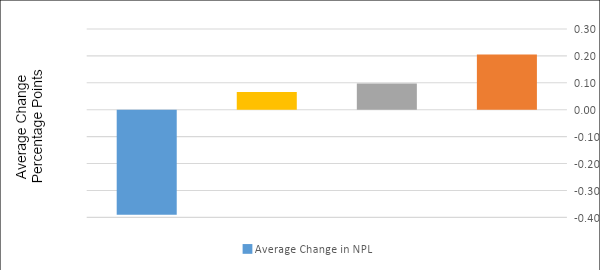

The pandemic affected debt repayment rates, with banks recording the highest rates of repayment deferrals as part of the measures introduced to alleviate the direct economic pressure that households and firms have come under during the pandemic. The following figure shows the changes in non-performing loan ratios, by country income group, over the years 2020-2021.

Figure 2: Changes in non-performing loan ratios, by country income group, 2020-2021

III- Restructuring Firm and Household Debt

According to the World Bank data, in countries with a normal bankruptcy system, it takes an average of more than two years to resolve a company’s bankruptcy case. Complex liquidations may take longer in case of an increase in over-indebtedness, even with efficient judiciary. Amid absence of effective legal mechanisms to declare bankruptcy or resolve creditor-debtor disputes, political interference in the credit market may be required. As such, improving the institutional capacity to manage insolvency becomes critical for equitable economic recovery for several reasons pertaining to the increased access to credit, faster creditor recovery, stronger job preservation, higher productivity, and lower failure rates for small businesses.

IV- Lending during Recovery and Beyond

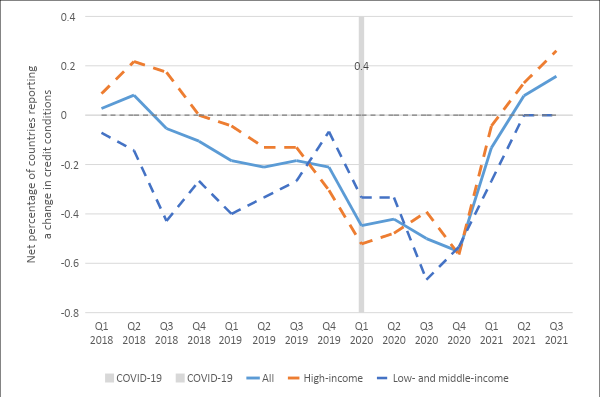

The ongoing impact of the Covid-19 on business performance and household incomes could inhibit new lending because of the increased credit risk. However, credit can be kept flowing by better visibility into borrower viability and improved recourse in the event of default, along with innovations in digital finance and reassessment of credit models to take into account the “new post-pandemic normal”. Additionally, regulatory frameworks that enable innovation can support credit in the recovery period while ensuring consumer and market protections.

Figure 3: Quarterly trends in credit conditions, by country income group, 2018-2021

V- Managing Sovereign Debt

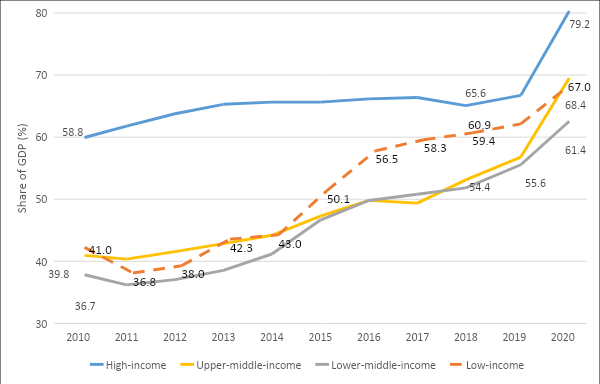

Covid-19 forced emerging and developing economies to expand their sovereign debt to record highs in an effort to mitigate the economic consequences of the crisis on households and their local economies. This contributed to an increase in the average total debt burdens among low- and middle-income countries by about nine percent of GDP during 2020, relative to an annual increase of 1.9 percent of GDP per year over the previous decade as is shown in figure 4.

Figure 4: Change in general government gross debt, by country income group, 2010-2020

The accumulation of sovereign debt poses significant risks to the global economic recovery, as debt-ridden governments fail to spend on public utilities, such as education and health care services, which would aggravate inequality and the human development outcomes. Further, countries in debt distress have limited capacities to deal with future shocks and may be unable to become the lender of last resort to private sector firms in need of public assistance.

In short, the Covid-19 crisis has exacerbated the economic risks facing countries. However, it offers a great opportunity to accelerate the shift towards a more efficient and sustainable global economy. In addition to the pandemic, there is climate change, a global phenomenon that has more severe impacts on low-income countries by exacerbating the existing vulnerabilities in these countries, such as the lack of access to clean water, low crop yields, food insecurity, and unsafe housing.