In times of crises and insecurity, the informal sector often becomes a resort to many workers rendered jobless during economic downturns. By definition, the informal sector is not monitored by governments. Unlike other crises, the pandemic has had an uneven impact on both the formal and informal sectors, leaving many workers in the informal economy in a much worse situation given their lack of social insurance coverage and other contributory protection.

First: How the informal sector has been faring during Covid-19

According to the World Bank report in May 2021, titled “The Long Shadow of Informality: Challenges and Policies”, the informal economy accounts for one-third of the economic activity in emerging markets and developing economies (EMDEs). In addition, 70 percent of job opportunities in these economies is provided through the informal sector, of which 50 percent is informal self-employment.

Women and young workers, particularly the lower-skilled, represent the larger proportion of informal workers, which makes them more vulnerable to losing their jobs, probably their only source of income in the absence of their ability to benefit from social safety nets. The informal sector is concentrated in the services industry where 72 percent of total firms in the services sector are informal.

Informality constraints governments’ ability to provide support during recessions, causing them to provide less support than their formal counterparts of developing or low- and middle-income countries. For example, in EMDEs with above-average informality, government revenues-to-GDP is approximately 5 to 12 percentage points below those of emerging markets and developing economies with low-average informality where government revenues account for 20 percent of GDP. Higher Informality was also associated with a decline in public spending by 10 percent due to the pandemic and inability of central banks in those countries to effectively provide support due to inefficiency of the financial system. Further, the informal sector makes lockdowns and social distancing challenging as informal employers and employees, with limited to no savings, can’t afford to stay at home otherwise they would lose their only source of income.

Second: Informality in the Middle East and North Africa

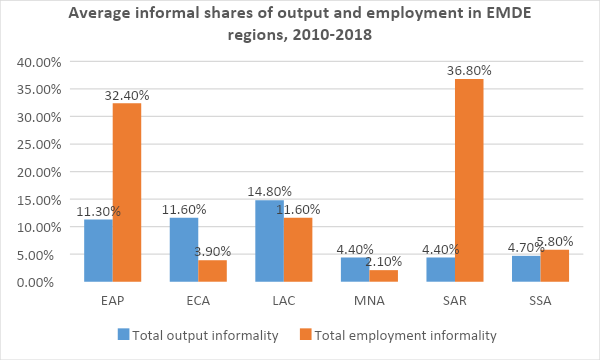

Figure 1: Average informal shares of output and employment in EMDE regions*, 2010-2018

Source: “The Long Shadow of Informality: Challenges and Policies” report, World Bank, May 2021

* EAP = East Asia and Pacific; ECA = Europe and Central Asia; LAC = Latin America and the Caribbean; MNA = Middle East and North Africa; SAR = South Asia; SSA = Sub-Saharan Africa

As shown in Figure 1, during the period 2010-2018, EMDEs in the MNA region had the least informality output and employment share accounting for only 4.4 percent (along with South Asia) of the average global informality output rate and 2.1 percent of the average informality employment rate.

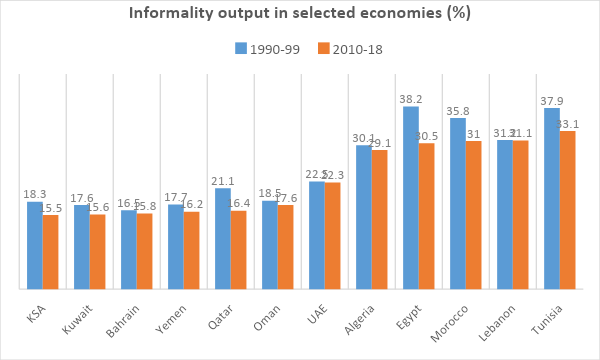

Figure 2: Informality output in selected economies (%)

Source: World Bank, May 2021

During the period 2010-2018, the average output informality share of total GDP in the MNA region amounted to 22 percent whereas the average informality employment share to total employment in the region during the same period stood at 23 percent. While Egypt was the country with the highest informality output in the region during the period 1990-1999 at a rate of 38.2 percent, it managed to bring this proportion down to 30.5 percent during the period 2000-2018 –a decrease of 7.7 percent considered the highest globally.

Looking at Gulf Cooperation Council (GCC) countries, we find that the informal activity in these countries is low compared to non-GCC countries. During the period 2010-2018, informality employment averaged only 3 percent of total employment in GCC countries, which is in line with the high per capita incomes in these countries. Several factors contribute to this low informal activity in GCC countries including their primary dependence on expatriate employees or high employment rate in the public sector.

Generally, the size of informal economy depends on a variety of factors including 1) quality of governance and efficiency of government services provided to registered firms (especially in sectors with a high potential to operate informally such as the service sector), 2) Ease of the registration processes, 3) quality of the tax system and tax rate, and 4) access to finance. According to the World Bank report, the efficiency of governments in non-GCC countries is worse than the average efficiency of governments in EMDEs. This is particularly true of the period between 2010 and 2018. However, according to the World Bank’s Enterprise Surveys (ESs) Indicators Data, 91.4 percent of firms operating in Egypt in 2016 were officially registered upon starting operations.

Figure 3: Government effectiveness and regulatory quality in selected non-GCC countries in the MNA

Source: World Bank Governance, 2021

Effectiveness of governments in non-GCC countries in the MNA region has also deteriorated. According to Enterprise ESs data, the average government effectiveness index for 2018 stood at a below average of -0.9 points (-2.5 weak; 2.5 strong), down from -0.5 in 2010. This value is also below the EMDE’s average of -0.4 recorded in the period 2010-2018. As for the regulatory quality, it averaged -1 in 2018 down from -0.6 in 2010 whereas the EMDE average stood at 0.4 in the period from 2010-2018.

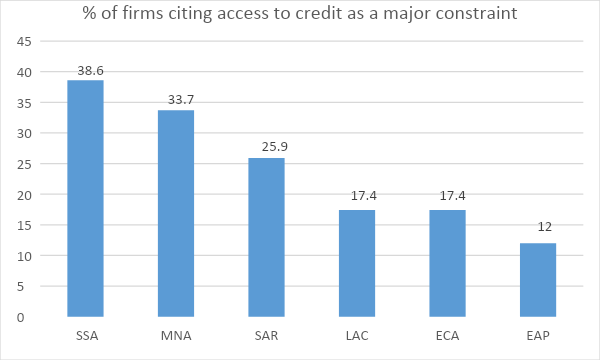

Figure 4: % of firms citing access to finance as a major constraint

Source: Enterprise Surveys Indicators Data, World Bank

The World Bank’s ESs data indicate that, the MNA region, excluding GCC countries, is the second largest region in terms of the number of companies that see access to finance as a major obstacle accounting for 33.7 percent of total respondents (second to Sub-Saharan Africa which have a percentage of 38.6 percent). This is indicative of the inefficiency of the fiscal system and the limited financial government contributions in the region.

One of the significant negative impacts of growth of the informal sector is that it undermines fair competition in the market. World Bank’s ESs data for Egypt show that 32.6 percent of respondents on the 2013 survey and 22.7 percent of the 2016 survey say that practices of informal competitors stood as an obstacle to them.

Overall, informality makes implementing lockdowns and controlling the spread of the pandemic challenging. It also has huge repercussions on government revenues and the governments’ ability to provide support, which may cause extreme poverty rates and income inequality, among other negative impacts. Countries’ efforts to reduce tax burdens, adopt modern technologies for e-payment and e-collection (e.g. Egypt), and create harmonized electronic filing systems (e.g. Morocco), have contributed to reducing the cost of the formal sector and adversely increasing the cost of the informal sector, which contributed to reducing the size of the sector.