Several African and Arab governments are striving to stimulate development and construction to mitigate the repercussions of the unrest and turmoil that have been experienced over the past decades.

In this vein, Egypt is keen to provide its expertise in fields of development and reconstruction for fraternal states to speed up the pace of development in these countries. To that end, Egypt works to push national construction companies to access regional markets to contribute to the reconstruction of what was devastated by wars and armed conflicts over the past decades and participate in the construction of hundreds of new economic and service projects that will help boost national economies and raise the quality of life for the public.

Promising Opportunities

Most regional Arab and African countries are aspiring to accelerate their development plans to keep pace with the emerging economies worldwide. Towards that, these countries direct a significant share of their investments to developing infrastructure that serves the economy and trade sectors, including the construction of roads, airports seaports, railways, and energy production facilities such as hydroelectric dams, solar cell plants, and thermal plants, as well as developing service buildings such as hospitals, health care centers, schools, business administration headquarters, and technology development centers.

The desire of these countries to develop their economic situation was driven by the relative security and political stability the Arab and African countries are witnessing after years of heightened armed and terrorist activity and the transition of the ruling regimes in those countries to recovery after experiencing extreme vulnerability due to the successive revolutions and waves of turmoil that were about to cause some countries to fall and others to fail.

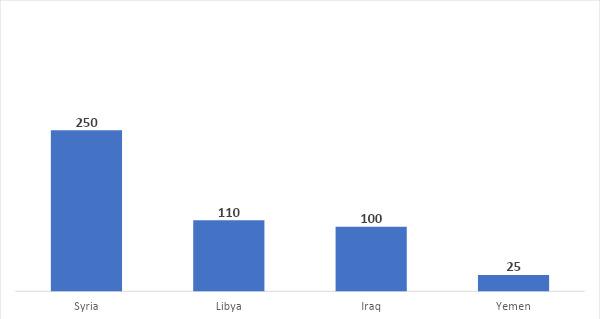

Data indicates that the costs of developing infrastructure and reconstruction projects in the Arab world and Africa are estimated at thousands of billions of dollars. The Arab countries that have suffered armed conflicts such as Libya, Iraq, Yemen, and Syria are to start reconstruction operations that will extend over medium and long-term intervals. The total cost of these operations is expected to reach more than $480 billion as is shown in figure 1.

Figure 1: Estimates of reconstruction costs in countries affected by security and military tensions over the past decades ($ million)

Sources: Syria, the 2018 World Bank estimates, Libya; estimates of the Libyan government in 2021, Iraq; the 2021 Iraqi Contractors Union data, Yemen; the 2020 World Bank estimates.

Additionally, several regional countries with powerful economies will implement huge projects to develop their infrastructure, including Saudi Arabia that seeks to invest $420 billion in supporting infrastructure and transport facilities throughout the Kingdom by 2030, more than 47 percent of these investments will go to the creation of smart cities.

Africa has the larger share of infrastructure investments. According to the management consulting company McKinsey, until 2025, several construction projects are planned to be implemented in numerous African countries with a value of up to $2.5 trillion. Data from the African Federation for Construction Contractor’s Associations (AFCCA) states that the steady increase of Africa’s population, expected to reach nearly 2.5 billion people by 2050, will increase the demand for new housing units by 10 million units annually.

Powerful National Companies

The urban boom that Egypt has witnessed since 2014 has stimulated many local investors to get into the construction contracting industry. Currently, there is more than 20,000 companies registered on lists of the Egyptian Federation for Construction and Building Contractors (EFCBC), which classifies companies into seven different categories based on a set of criteria, including the company’s business volume, its capital, years of experience, the work force, and the monetary value of its equipment.

The majority of these contracting companies are classified as nascent, small, or medium-sized. In other words, 80 percent of Egyptian contracting companies come on the bottom four ranks of the EFCBC classification. However, there are 3,000 major Egyptian companies ranked within the first, second, and third categories of the EFCBC classification. These companies have a track record of substantial success, let alone many other qualifications required to work on international projects.

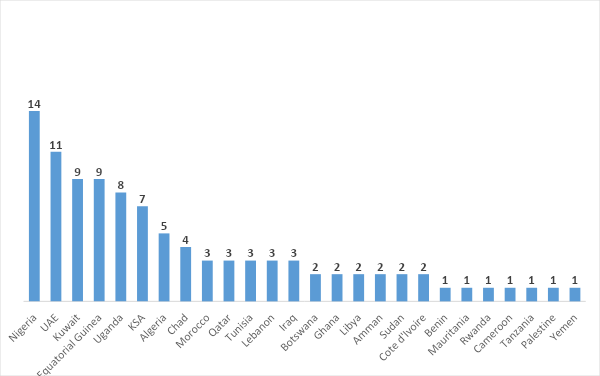

The Arab Contractors (AC) company of the public sector is one of the most successful companies among the major construction companies in Egypt. Over the past 65 years, the company has managed to penetrate 26 Arab and African markets, successfully implementing more than 100 projects as is shown in figure 2. At large, these projects have been characterized by diversity, ranging from the construction of dams, hydroelectric power stations, land roads, and sea and air ports to the construction of service buildings, government departments, and the basic facilities.

A prominent project of the AC in Africa is the Julius Nyerere Hydropower Plant and Dam, which is being implemented in collaboration with El Sewedy Electric. Upon completion, the dam is expected to have an installed annual capacity of 6,307 megawatts/ hour, which would help provide electricity to 17 million Tanzanian families. The Expansion and Development of the Port of Tripoli is another major overseas project implemented by the Arab Contractors. The project is projected to increase the port’s cargo capacity to receive about 5 million tons of cargo a year, i.e. a 500 percent increase over the pre-expansion capacity.

Other significant examples of overseas construction and infrastructure projects implemented by the AC include the project of developing the road network around the Chadian capital, N’Djamena, at a length of 186km and developing the sewage system in Sidon, at a length of 141 km along with its annexed treatment plant.

Figure 2: Projects implemented by the AC in African and Arab countries

Orascom constructions, a private sector company, is another powerful Egyptian company engaged in construction and contracting works outside Egypt. Besides its domestic projects (now numbering 27 projects), the company is currently implementing 23 international projects, 6 of which are in Arab countries, including the UAE, Algeria, Bahrain, and KSA, the most significant of which was the development of Hamma Seawater Desalination Plant in Algeria which has a daily capacity of 200,000 cubic meters of desalinated water. Over the coming period, the company intends to expand its regional business, by penetrating into several sub-Saharan markets, particularly countries with high populations, such as Ghana, Senegal, Tanzania, and Kenya.

El Sewedy Electric is another leading construction company in Egypt. The company specializes in the construction of power stations. Over the past years, El Sewedy managed to implement 25 different projects that involved the installation and commissioning of overhead transmission lines in African and Arab countries, including Saudi Arabia, Algeria, Zambia, Ethiopia, Ghana, and Tanzania. Additionally, the company managed to land several civil engineering in a number of fraternal countries, including tender for the construction of 46 bridges and 8 culverts over the Bordj Bou Arreridj-Setif Autoroute and the construction of 7 groynes and rehabilitation of existing sea walls, groynes and revetments in Mozambique.

Heated Competition

The multiplicity of development opportunities in Africa and the Middle East have spurred many countries to seek attracting the largest share of contracting investments. This fierce competition manifests itself best in Africa where the competition between exporters of construction services intensifies. According to the Africa Construction Trends Report by Deloitte Touche Tohmatsu Limited’s (DTTL), 385 major construction projects were implemented in Africa in 2020 with a total project value of $399 billion.

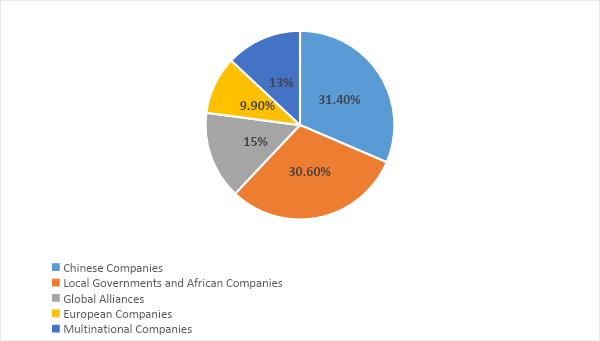

Several contracting companies competed for these projects including contracting companies from major countries, emerging economies, and local African countries. Figure 3 shows construction companies’ acquisition share of major projects in Africa in 2020 by company nationality. As the figure indicates, Chinese companies got the lion’s share of these investments, implementing 31.4 percent of the total construction projects in Africa, followed by local governments and African companies which got their hands on 30.6 percent of the projects and global alliances (between African and international companies) which acquired 15 percent of the projects. European companies, however, only got their hands on 9.9 percent of construction projects in Africa, whereas other companies from the United States, Russia, the United Kingdom, Turkey, Australia, Japan and South Korea, only succeeded in obtaining a total of 13 percent of the total projects.

Figure 3: Construction companies’ acquisition share of major projects in Africa in 2020 by company nationality

In the Middle East, there is growing competition between regional and international construction companies. Iraq is a case in point. It is an arena for competition among construction companies. Given the urgent need to develop all infrastructure facilities in the country that has been neglected for nearly 20 years and the pressing need for the reconstruction of cities and regions ravaged by terrorist groups during the past decade, the Iraqi government has undertook several initiatives to provide the necessary funding for these costly development operations.

Among these initiatives was Iraq’s calling for international partners to provide the financial and technical support that Iraq needs through some international forums and establishing an oil-for-reconstruction mechanism with a number of friendly countries to avoid depleting the state’s financial liquidity. By adopting this mechanism, Iraq managed to attract companies from Egypt and China to implement the required development projects; however, several regional countries such as Iran and Turkey are exerting pressure on the Iraqi authorities to obtain shares of development projects in the country. A number of major countries from the United States and the European Union are seeking to dislodge China and get the projects Beijing implements in Iraq.

Steps to Consolidate Egypt’s Construction Industry

There are numerous opportunities for Egyptian construction companies to expand their business in markets of fraternal Arab and African countries. However, the huge scale of competition that requires taking integrated steps to strengthen the position of the Egyptian contractors, towards acquiring a good share of the Arab and African construction market.

First, there is a need to develop an integrated strategy for the export of construction services to the Arab and African countries. Such a strategy would contribute to coordinating the efforts of active actors in the industry, whether government agencies or public and private institutions. This, in turn, would strengthen capabilities of the Egyptian construction sector against external competitors and promote integration among them in the event that projects require various technical specializations.

Further, the government can also develop incentive programs for small and medium enterprises working in the construction field, estimated at more than 16,000 companies, towards developing their capabilities over time, which will later qualify them to match international standards, enabling them to work on external projects. Additionally, manufacturers of construction materials can be integrated into any prospective construction export strategy to capitalize on the capabilities of Egyptian industries in implementing overseas projects, which brings double benefits to the national economy.

Beyond that, Egypt should continue its political endeavors geared towards concluding agreements and protocols with fraternal countries in the Middle East and the three African economic blocs, to facilitate the exit and entrance of Egyptian companies, their personnel, and equipment into target markets, and remove all administrative and financial restrictions that may disrupt or limit their work. Furthermore, the government should pursue its existing plans to promote foreign trade representation offices, which would make it easy for national companies to obtain the required information on the development projects put forward or under-consideration in different countries and help them overcome potential obstacles in project implementation.

At the financial level, the competent authorities must work on the provision of a large network of national banks in the target countries of the construction export strategy. Branches of national banks in these countries would facilitate bank transfers and the issuance of letters of guarantees, ensuring speed and flexibility for contracting companies to complete their work.

Finally, promoting the construction industry in the targeted countries should be borne in mind when developing construction export strategies to highlight the capabilities of our companies, clearly demonstrated in the implementation of hundreds of construction projects inside and outside Egypt over the past few years. The government should also consider organizing international exhibitions in the countries targeted in the export strategy, to ensure direct communication between potential customers and representatives of national contracting companies.