The outbreak of the coronavirus pandemic and its negative repercussions on world economies resulted in full or partial lockdown across the world, causing many economic activities to stop and investment risks to increase.

The lockdown brought about a slowdown in established investment projects, a sharp fall in investment flows, and a marked reluctance of venture capitalists to risk their money.

Furthermore, the decline in domestic investments was accompanied by a sharper decline in foreign direct investment (FDI) flows devastated by the impact of the pandemic on foreign exchange sectors including tourism, international trade, and foreign investment.

To alleviate the consequences of the crisis and address impacts of the pandemic on the economy, the government adopted several financial, monetary, and social policies that help catalyze domestic and foreign direct investment flows to increase economic growth rates.

The outcome has been Egypt’s economy retaining a positive growth rate of 3.57 percent during fiscal year 2019-2020 as world economies were suffering negative growth rates.

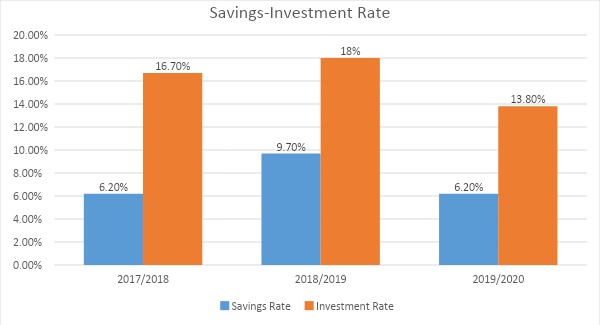

Domestic savings-investment gap

Under Egypt’s Vision 2030, Egypt targets increasing domestic investment share to account for 30 percent of gross domestic product (GDP). This investment demand was planned to be funded through domestic savings. However, Egypt’s economy faces a wide investment-savings gap, i.e. domestic savings are lower than domestic investment. This gap could be attributed to the increase in marginal propensity to consume (MPC) and the negative government savings due to the high budget deficit. The following figure shows savings and investment rates in Egypt over the period 2017-2020. While the savings-investment gap remained large during the review period, it went down from 10.5 percent in 2017-2018 to 7.6 percent in 2019-2020.

Figure 1: Savings-investment rate

In 2019-2020, interest rates declined to promote and attract investment, but the step backfired, leading to a decline in both savings and investment rate. The savings rate is measured by the amount of money that isn’t spent from the total disposable income.

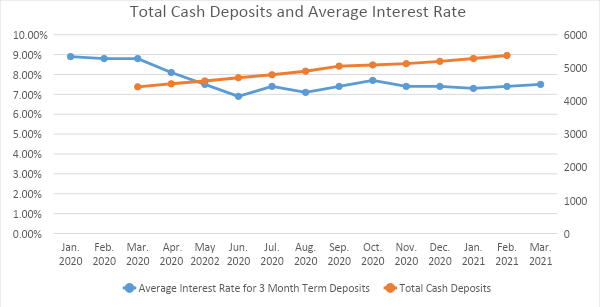

Despite the decline in interest rates, individuals’ savings were directed to cash deposits. The uncertain economic situation and the high risks related to other aspects of investment in an environment characterized by a declining economic activity may have contributed to this trend as is indicated in Figure 2 showing a positive correlation between the reduction in interest rates and the increase in cash deposits.

Egypt’s financial policies, economic facilitation programs, irregular employment assistance, and the Central bank of Egypt’s (CBE) initiatives that allow for postponement of loan dues for individuals and small and medium enterprises affected by the pandemic, led to an increase in the total disposable income, the bulk of which went to consumption spending, i.e. the total disposable income had been greater than savings due to an increase in the MPC which negatively affected savings rate.

Figure 2: Total cash deposits and average interest rate

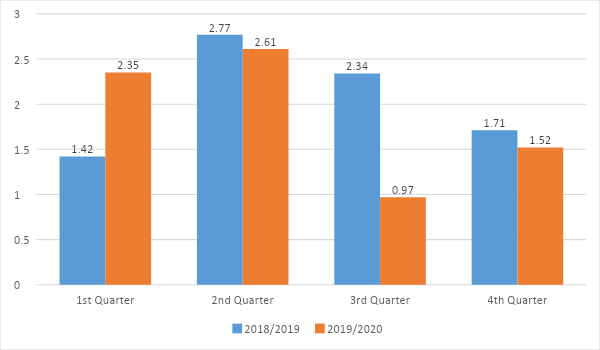

Fiscal year 2019-2020 witnessed a decline in the volume of implemented investments and their share of GDP. That year, the total implemented investments-to-GDP amounted to 13.7 percent, down from 17.3 percent in 2018-2019, despite the increased government investments in infrastructure projects and major national projects.

Figure 3: Total implemented investments share of GDP

Overall, the savings-investment gap requires greater effort to attract foreign investments which would help raise the economy’s capacity to finance its investments.

FDI in Egypt

The year 2019-2020 saw a decrease in the total FDI inflows by 3.4 percent to record about $15.8 billion, down from about $16.4 billion in 2018-2019. However, the total FDI outflows increased by 2.8 percent to record about $8.4 billion, up from about 8.2 billion in the previous year. This resulted in a decrease in Egypt’s net FDI by 9.5 percent totalling about $7.5 billion, compared to about $8.2 billion for the previous year.

This trend continued during the first half of the year 2020-2021 where the net FDI inflows decreased by 32.3 percent to record about $3.4 billion, down from $5 billion during the first half of the previous year.

Figure 4: Net FDI in Egypt ($ billion)

Nevertheless, such decline in FDI in Egypt during the year 2019-2020 and the first half of 2020-2021 wasn’t out of left field. According to reports by the United Nations Conference on Trade and Development (UNCTAD), Egypt has always been the largest recipient of FDI in Africa; however, the pandemic caused a sharp decline in FDI inflows to Egypt.

Data from the General Authority for Investment and Free Zones (GAFI) show a slight decline in new business formation, where new business established in 2019-2020 amounted to 22,033 with an issued share capital of EGP 83.8 billion compared to 22,359 new businesses in 2018-2019 with an issued share capital of EGP 57.3 billion. During the period from January to April 2021, the number of new businesses established amounted to 9,434 businesses with an issued share capital of EGP 31.3 billion, up from to about 6,778 businesses with an issued share capital of EGP 22.7 billion during the same period in 2020, i.e. an increase of 39.2 percent and 38 percent in number of new businesses and issued share capital respectively.

With Egypt adopting the Economic Reform Program 2016-2022, numerous measures were taken to stimulate and attract investment, ranging from legislative reforms and enactment of investment legislation including the Investment Law No. 72 of 2017, to automation and digitization of GAFI’s services, launching an industrial investment map, addressing obstacles that face investors, and resolving investors’ disputes through the Ministerial Committee for the Settlement of Investment Disputes. Further, a number of investor service centers (ISCs) have been opened in governorates, bringing the total number of ICSs to 12 centers located in Cairo (headquarters), 10th of Ramadan city, 6 October city, Alexandria, Gamasa, Port Said, Sharm Al-Sheikh, Qena, Sohag, Assiut, Minya, and Ismailia. Free zones have had their share of development as well where 9 public free zones have been developed in Alexandria, Nasr City, Port Said, Ismailia, Damietta, Suez, Shebin Al-Kom in Menoufia, Qift in Qena, and the media public free zone in 6th of October. Moreover, a comprehensive plan for infrastructure rehabilitation and constructing roads and facilities necessary for attracting and facilitating investments have been implemented, and work on all of these projects progressed on through the pandemic year. Also, during the pandemic year, the CBE adopted an expansionary monetary policy that included cutting interest rates to reduce the cost of investment and postponing loan dues for individuals and enterprises for 6 months without imposing late payment penalties to provide cash for businesses, ensure operational continuity, and minimize chances of stymieing investments. The CBE also launched a number of initiatives to support the most affected sectors including tourism, industry, agriculture, and construction, besides offering tax incentives provided for in the new Law on the Development of Micro, Small and Medium Enterprises.

In summary, the decline in investments in Egypt was caused by the repercussions of Covid-19 that resulted in an economic downturn, a halt in economic activities, and heightened risks. However, Egypt’s legislative and institutional reforms and efforts to improve the investment climate paid off during the year of the pandemic, limiting the decline in investments and promising more investment inflows in the upcoming years amid continued improvement of the investment climate.