International trade has undergone rapid transformations in recent years, reflecting a deeper shift in the nature of the global economic order. Trade is no longer managed solely according to considerations of economic efficiency and market liberalization; rather, it has become increasingly linked to national security, supply chain resilience, and geopolitical competition. Within this context, American trade policy—particularly during 2025 and continuing through 2026—has emerged as a clear manifestation of this transformation through the expanded use of tariffs, the integration of strategic considerations into trade policy, and efforts to reshore critical industries within the United States.

The significance of these developments extends beyond the historic ruling issued by the Supreme Court of the United States on February 20, 2026, which limited the authority of the American president to impose tariffs. Rather, they reflect a broader trend toward restructuring the very foundations of the global trading system. This report therefore examines not only the implications of the judicial ruling or American protectionist policies, but also analyzes how the growing use of trade protection instruments and the restructuring of supply chains have driven countries to accelerate trade agreements and reposition their economic relationships. These developments illustrate a broader shift in international trade from a primary focus on economic efficiency toward an increasing emphasis on resilience, economic security, and risk management.

These transformations have coincided with growing uncertainty regarding the stability of the global trading system, particularly following judicial developments related to American tariffs and the subsequent rapid efforts to employ alternative legal and trade mechanisms. At the same time, many countries have accelerated the pace of bilateral and regional trade agreements, not only to expand trade exchange, but also to secure supply chains, diversify partnerships, and reduce exposure to geopolitical and economic risks.

Against this backdrop, examining the implications of the restructuring of the global trading system for emerging economies—foremost among them Egypt—has become increasingly important. This includes assessing the impact of new trade agreements on Egypt’s competitiveness, as well as evaluating the nature of the trade and regulatory challenges shaping its economic relations with the United States. Accordingly, this report seeks to analyze the transformations in American trade policy, examine the accompanying international developments, and assess the challenges and opportunities these changes present for the Egyptian economy.

First: American Trade Policy in 2026

The 2026 American Trade Policy Agenda issued by the Office of the United States Trade Representative reflects a clear transformation in the philosophy governing international trade management. The United States no longer views trade solely as a tool for maximizing economic efficiency, but increasingly as a direct mechanism for rebuilding the domestic production base and strengthening national security. The adoption of the “America First” approach is therefore no longer merely a political slogan, but has evolved into a governing framework that restructures trade policy priorities around domestic production, reducing the trade deficit, and linking trade policy to strategic considerations.

This transformation is rooted in an assessment by the American administration that the country faces a deep and prolonged structural crisis characterized by chronic trade deficits and the erosion of the industrial base as a result of decades of debt-driven consumption and unequal economic openness with trading partners. Accordingly, the new policy seeks to restore balance between production and consumption by steering the American economy toward producing what it consumes rather than financing imports through expanding borrowing.

Within this framework, the 2026 American Trade Policy Agenda focuses on a set of integrated priorities, including expanding reciprocal trade agreements, strengthening the enforcement of trade laws, and securing supply chains in strategic sectors such as pharmaceuticals, minerals, and energy. It also includes reassessing existing agreements such as the United States–Mexico–Canada Agreement and managing trade relations with China on the basis of “reciprocity.” More broadly, the agenda reflects a shift toward redefining the rules of the international trading system itself in ways that allow greater flexibility in differentiating among partners according to strategic considerations.

In this context, trade policy instruments—most notably tariffs—are no longer viewed merely as traditional protectionist tools, but rather as components of a broader strategy aimed at redirecting global supply chains and strengthening domestic manufacturing. This explains the actions undertaken by the American administration following the judicial ruling, as well as its rapid recourse to alternative legal mechanisms in order to preserve its protectionist approach.

At the same time, these transformations, combined with the growing uncertainty surrounding the stability of trade policy even within the world’s largest economy, have encouraged many countries to accelerate the negotiation and expansion of trade agreements. The purpose of these agreements is no longer confined to reducing tariffs, but has expanded to include securing supply chains, diversifying partnerships, and managing risks within an increasingly volatile international environment.

Accordingly, current developments in international trade can be understood through two parallel dynamics: the first is led by the United States through the use of flexible protectionist instruments aimed at reshaping the global economy in line with American interests, while the second is led by other countries through the construction of networks of trade agreements designed to enhance resilience and reduce exposure to geopolitical and economic risks.

Second: US Measures Following the Supreme Court Ruling

The measures adopted by the United States following the historic ruling issued by the Supreme Court of the United States on February 20, 2026—which limited the authority of the American president to impose tariffs—demonstrate that the administration of Donald Trump did not move toward retreat, but rather toward rapid repositioning through the use of alternative legal instruments. The swift activation of “Section 122” and the imposition of temporary tariffs indicate that the ruling was not entirely unexpected, and that there had been prior preparation to address it through a “contingency plan” designed to preserve the protectionist approach. This step was not an objective in itself, but rather a transitional mechanism intended to buy time until more firmly established legal pathways—such as Section 232 related to national security, or Section 301 concerning unfair trade practices—could be activated.

The more significant development, however, lies not only in the legal instrument employed, but also in the evolving nature of trade policy itself, which has shifted from the imposition of conventional tariffs toward what may be described as a “graduated tariff system.” This became evident in the April 2026 decisions concerning strategic minerals, in which the American administration not only raised tariffs to 50 percent on steel, aluminum, and copper, but also altered the method of calculation so that tariffs were imposed on the full value of the product rather than only part of it, thereby reducing opportunities for evasion or circumvention.

Moreover, the tariff structure is no longer uniform, but increasingly tiered according to economic and political considerations. Higher levels of protection are applied to core products, lower rates to derivative products, and reduced tariffs to goods incorporating American inputs. In some cases, partial or full exemptions are granted. This graduated structure reflects a clear objective: redirecting global supply chains so that they become more dependent on production within the United States, or at minimum on American-made inputs.

This orientation is even more evident in the pharmaceutical sector, where an exceptionally flexible and complex tariff regime has been established. Tariffs reaching up to 100 percent have been imposed on patented medicines. At the same time, however, substantial incentives have been offered to companies willing to relocate production to the United States, including tariff reductions to 20 percent or even full exemptions in cases where companies commit to domestic production and pricing agreements. Certain allied economies, such as the European Union, Japan, and South Korea, were granted lower tariff rates, while the United Kingdom received more preferential treatment. Some sensitive categories, such as orphan drugs, were also exempted.

This broad tariff range—from complete exemption to 100 percent—demonstrates that tariffs are no longer merely financial instruments, but have become mechanisms for managing the behavior of both corporations and states. They are increasingly used as incentives for those aligning with American priorities, and as pressure tools against those resisting them, particularly with regard to the localization of industrial production.

Within the same context, threats to raise tariffs on European automobiles to 25 percent, while linking exemptions to domestic production within the United States, further confirm that the central objective of trade policy is no longer simply reducing imports or increasing revenues, but rather redistributing global production locations. In other words, tariffs are being used to encourage foreign companies to relocate manufacturing operations to the American market.

These policies represent a clear transformation in the role played by tariffs. They are no longer merely traditional protectionist measures, but have evolved into flexible instruments continuously employed to restructure supply chains, stimulate domestic investment within the United States, and strengthen sectors linked to national security. Furthermore, the diversity of legal foundations underpinning these measures grants the administration greater room for maneuver and makes it more difficult to challenge such policies in the same manner that hindered earlier decisions.

Third: International Responses Following the US Supreme Court Ruling

On the other side of the transformations in American trade policy, the map of international trade agreements following the ruling of the Supreme Court of the United States reveals a parallel trend of equal importance: the accelerating movement by countries toward concluding new agreements or upgrading existing ones, not merely to enhance trade, but as a direct response to an international environment characterized by rising uncertainty. Even with the judicial constraints imposed on certain American tariff instruments, the broader sense of instability has not diminished. On the contrary, it has reinforced the perception among states that the global trading system has become increasingly vulnerable to political and legal fluctuations, prompting them to seek more stable and flexible alternatives. This trend can be observed through the following agreements and initiatives:

- The Free Trade Agreement Between New Zealand and India

Under this agreement, a substantial portion of New Zealand’s current exports will either become exempt from tariffs or subject to reduced tariff rates. More than half of these exports will receive immediate full tariff exemptions once the agreement enters into force, while this preferential coverage will expand to encompass more than 80 percent of exports upon the agreement’s full implementation.

At its core, this agreement reflects an effort to geographically redistribute trade relations. The move toward a market the size of India is not driven solely by economic opportunity, but also by the desire to reduce dependence on traditional partners, particularly amid intensifying international competition for access to major markets. Consequently, trade liberalization in this context becomes part of a broader strategy for diversifying risk rather than an objective in itself.

- The Free Trade Agreement Between the European Union and Mercosur

At the level of major economic blocs, the provisional implementation of the European Union–Mercosur agreement represents a strategic step toward reshaping the global trade landscape. Although the agreement appears conventional in terms of reducing tariff barriers, its true significance lies in its role as a mechanism for diversifying partnerships and securing access to natural resources, particularly as Europe seeks to reduce dependence on limited sources of supply.

Furthermore, the inclusion of issues such as climate policy and labor rights reflects the expansion of trade agreements beyond the traditional exchange of goods into broader regulatory and strategic dimensions.

- The AOTES Agreement Between New Zealand and Singapore

Within this context, the AOTES agreement (Agreement on Trade in Essential Supplies) between New Zealand and Singapore represents an advanced model of this transformation. The agreement moves beyond the traditional logic of “trade liberalization” toward the concept of “trade security” during times of crisis.

Rather than focusing primarily on reducing tariffs, the agreement establishes a legal commitment not to impose export restrictions on essential goods such as food, fuel, and medical supplies, even during emergencies. The significance of this step lies in the fact that it reflects a shift in state priorities—from maximizing trade gains under normal conditions to ensuring the uninterrupted flow of critical goods under exceptional circumstances.

Accordingly, this agreement may be viewed as part of a broader trend toward the establishment of “preventive agreements” designed to shield supply chains from future shocks.

- Agreements Signed Between Australia and Japan

In parallel with these developments, some agreements have moved toward directly integrating the security dimension into the core of economic cooperation, as reflected in the agreements signed between Australia and Japan. These agreements extend beyond trade and investment to encompass energy, critical minerals, and defense cooperation. This development reflects a clear transformation in the function of trade agreements, which are no longer viewed solely as economic instruments, but increasingly as components of a broader “economic security” framework through which states seek to reduce dependence on unreliable suppliers, particularly in strategic sectors such as rare minerals.

- The Agreement Between the European Union and Australia

This trend is further reinforced by the agreement between the European Union and Australia, which combines trade liberalization with efforts to secure supply chains for critical raw materials such as lithium and minerals linked to the green transition. Here, it becomes evident that trade agreements have increasingly evolved into instruments for achieving “industrial security,” rather than merely expanding trade exchange.

The agreement also reflects a broader European orientation toward strengthening its presence in the Indo-Pacific region, thereby supporting a strategy aimed at diversifying partnerships and reducing geographic risks.

- The Comprehensive Economic Partnership Agreement Between India and Canada (CEPA)

Within a similar context, the resumption of negotiations on the Comprehensive Economic Partnership Agreement (CEPA) between India and Canada represents an example of how trade agreements are increasingly being used as instruments for rebuilding both political and economic relations simultaneously. The agreement focuses not only on trade liberalization, but also on establishing institutional frameworks to ensure the continuity of cooperation, while prioritizing future-oriented sectors such as technology, clean energy, and critical minerals.

This reflects a growing tendency to link trade to political and security stability rather than treating it as a separate sphere.

From a broader perspective, the significant expansion of trade negotiations led by India with a range of countries can be understood as part of a “trade route diversification” strategy. Rather than relying on a limited number of partners, India is seeking to build an extensive network of agreements that provides greater flexibility in confronting future shocks. This approach reflects a growing recognition that dependence on a single, unified global trading system is no longer sufficient, and that countries increasingly need diversified networks to ensure the stability and resilience of their trade relations.

- The Trade Agreement Between China and Switzerland

In the same direction, China’s efforts to modernize its trade agreement with Switzerland reflect a broader transformation in the nature of trade agreements themselves, shifting from a primary focus on goods toward greater emphasis on services, technology, and digital trade. This development indicates that competition within the global trading system is no longer confined to the movement of goods, but has become increasingly linked to the digital economy and knowledge-based value chains. Consequently, countries are being driven to update their agreements in ways that align with these structural transformations.

Taken together, the aforementioned agreements reflect the responses of the principal actors within the international trading system to shifts in American trade policy. They reveal a clear pattern in which trade agreements are no longer merely instruments for trade liberalization, but have increasingly evolved into mechanisms for risk management within an unstable international environment.

As political and legal volatility intensifies within major economies, states have become more inclined to safeguard their interests through flexible bilateral and regional agreements capable of ensuring the uninterrupted flow of goods, supporting the diversification of partnerships, and strengthening resilience against future shocks. Accordingly, the accelerating pace of these agreements reflects not only a desire to expand trade, but more fundamentally an attempt to restore a degree of certainty within a global system moving toward greater complexity and instability.

Table (1): Summary of agreements and their Strategic implications

| Agreement | Main Focus | Strategic Implication |

|---|---|---|

| Free Trade Agreement between New Zealand and India | Tariff reduction and market access | Reducing dependence on traditional trading partners |

| Free Trade Agreement between the European Union and Mercosur | Trade and natural resources | A mechanism for diversifying partnerships and securing access to natural resources |

| AOTES Agreement between New Zealand and Singapore | Supply security during crises | Moves beyond the traditional logic of “trade liberalization” toward the concept of “trade security” |

| Agreements signed between Australia and Japan | Energy, critical minerals, and defense | Reflect a clear transformation in the role of trade agreements, which are no longer merely economic instruments, but have become part of a broader “economic security” framework aimed at reducing dependence on unreliable suppliers |

| Agreement between the European Union and Australia | Lithium and critical minerals | Trade agreements have increasingly become instruments for achieving “industrial security” |

| Comprehensive Economic Partnership Agreement (CEPA) between India and Canada | Technology, clean energy, and critical minerals | Linking trade to political and security stability while building diversified networks to ensure trade resilience |

| Trade Agreement between China and Switzerland | Services, technology, and digital trade | Competition within the global trading system is no longer confined to the movement of goods, but is increasingly linked to the digital economy and knowledge-based value chains |

Fourth: Implications for Egypt

- The Impact of Free Trade Agreements Among States on Trade and Investment in Egypt

The implications of the new wave of trade agreements extend beyond the redistribution of global trade flows to directly affect the competitive standing of various countries within the international trading system, including Egypt. For example, the expansion by the European Union—Egypt’s primary trading partner—in granting preferential advantages to major production blocs such as Mercosur may weaken the comparative advantage long enjoyed by Egyptian exports through preferential access to the European market, particularly in key sectors within Egypt’s export structure.

In this context, the challenges facing Egypt are not limited merely to price competition, but also stem from the transformation of global trade itself toward concepts centered on economic security, resilient supply chains, and environmental and technological compliance.

These transformations also extend to the transport and logistics sector, especially amid growing discussion surrounding the India–Middle East–Europe Economic Corridor as a strategic alternative to traditional trade routes. Although the project has faced setbacks due to regional tensions, the expansion of trade between India and Europe, particularly in light of the free trade agreement between the European Union and India in January 2026, has increased its economic significance, potentially posing a long-term challenge to traditional trade routes.

At the same time, Egypt may benefit from the expansion of trade flows between Asia and Europe through the Suez Canal corridor. However, the central challenge lies in Egypt’s ability to evolve from being merely a transit route into a key partner in supply chains, manufacturing, and logistics services associated with the emerging global trading system.

The new agreements also reflect a global trend toward linking trade with energy, supply chains, and environmental considerations. Within this framework, Egypt is positioning itself as a regional hub for green hydrogen, leveraging its geographic location and proximity to Europe. Nevertheless, competition is intensifying from countries such as India, which possesses a substantial industrial base and large-scale production capabilities supported by European partnerships.

- Trade Policy Between Egypt and the United States

First: Trade Exchange Between Egypt and the United States

Table (2): Trade Exchange Between Egypt and the United States

| Item | Goods (2025) | Goods (2024) |

|---|---|---|

| American Exports to Egypt | ||

| Value | $9.5 billion | $6.1 billion |

| Change | ▲ 55.5% (+$3.2 billion) | |

| American Imports from Egypt | ||

| Value | $2.9 billion | $2.7 billion |

| Change | ▲ 7.4% (+$0.2 billion) | |

| Trade Balance | ||

| American Surplus | $6.6 billion | $3.4 billion |

| Rate of Change | ▲ 94% | |

| Total Trade | $12.4 billion | |

| Egypt’s Ranking as a Market for American Exports | 37th | 37th |

Source: Trade Map

A notable shift has emerged in trade relations between the United States and Egypt during 2025, particularly in terms of the balance governing the economic relationship between the two countries, as the gap has widened rapidly in favor of the American side. In the trade of goods, the American trade surplus surged to $6.6 billion, marking an increase of 94 percent compared with 2024. At its core, this figure reflects an imbalanced equation: American exports to Egypt reached $9.5 billion, recording an increase approaching one-half within a single year, while American imports from Egypt did not exceed $2.9 billion, growing by only 7.4 percent.

Total trade exchange between the two countries reached approximately $12.4 billion, with Egypt ranking as the 37th largest market for American merchandise exports. Nevertheless, the figures clearly indicate a trade relationship that is significantly more oriented toward imports from the United States than toward Egyptian exports to the American market.

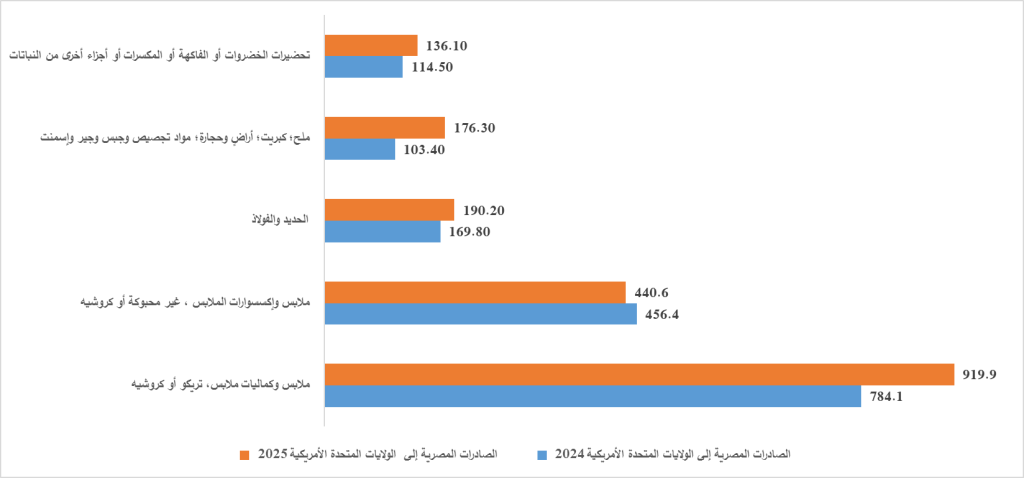

Figure (1): Main Commodity Groups Exported by Egypt to the United States in 2024 and 2025 (Million Dollars)

Figure (1): Main Commodity Groups Exported by Egypt to the United States in 2024 and 2025 (Million Dollars)

| Commodity Group | 2024 | 2025 |

|---|---|---|

| Preparations of vegetables, fruits, nuts, or other parts of plants | 114.5 | 136.1 |

| Stone, gypsum, cement, and related construction materials | 103.4 | 176.3 |

| Iron and steel | 169.8 | 190.2 |

| Non-knit apparel and clothing accessories | 456.4 | 440.6 |

| Knit or crocheted apparel and clothing accessories | 784.1 | 919.9 |

Source: Trade Map

The composition of Egyptian exports to the United States during 2025 reveals the continued relative concentration of Egyptian exports within a limited number of sectors, foremost among them the ready-made garments industry, which maintained its position as Egypt’s largest export category to the American market. Exports of knitwear and crocheted apparel increased from $784.1 million in 2024 to $919.9 million in 2025, recording a growth rate of approximately 17.3%. This reflects the sector’s continued benefit from the Qualified Industrial Zones (QIZ) Protocol, as well as the competitive advantage enjoyed by Egyptian products in the American market.

Exports of iron and steel also rose from $169.8 million to $190.2 million, marking an increase of 12%, while exports of prepared vegetables, fruits, and nuts grew by 18.9% to reach $136.1 million, indicating a relative improvement in certain Egyptian industrial and food exports.

Conversely, some export categories experienced declines. Exports of non-knit apparel and clothing accessories fell from $456.4 million to $440.6 million, reflecting a decline of 3.5%. Meanwhile, salt, sulfur, stone, and construction materials recorded the highest growth rate among the principal commodity groups, surging from $103.4 million to $176.3 million, an increase of approximately 70.5%. This development reflects growing American demand for certain Egyptian raw materials.

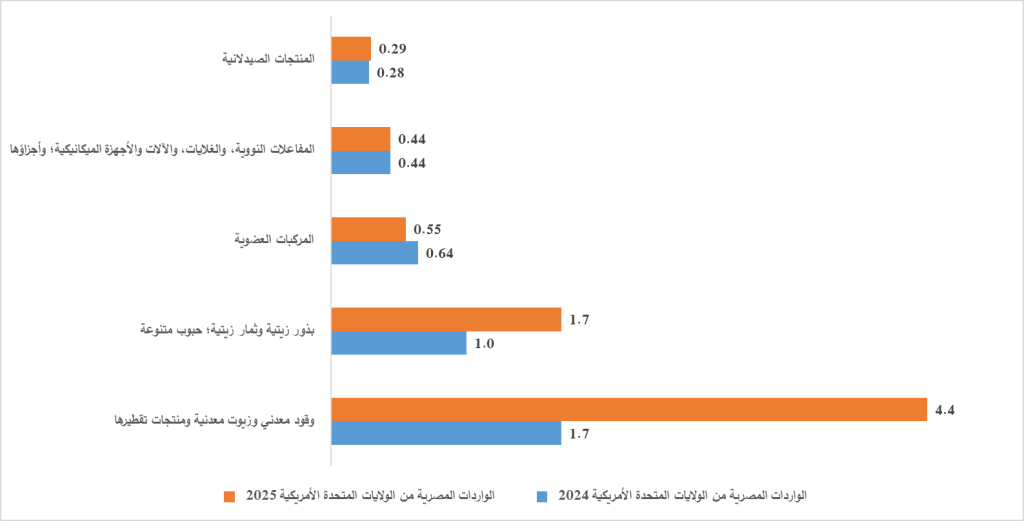

Figure (2): Main Commodity Groups Imported by Egypt from the United States in 2024 and 2025 (Billion Dollars)

| Commodity Group | 2024 | 2025 |

|---|---|---|

| Pharmaceutical products | 0.28 | 0.29 |

| Nuclear reactors, boilers, machinery, mechanical appliances, and parts thereof | 0.44 | 0.44 |

| Organic chemicals | 0.64 | 0.55 |

| Oilseeds, oleaginous fruits, and miscellaneous grains | 1.0 | 1.7 |

| Mineral fuels, mineral oils, and products of their distillation | 1.7 | 4.4 |

Source: Trade Map

On the import side, the data reveal a clear expansion in Egypt’s reliance on American goods, particularly in the energy sector. Imports of mineral fuels, mineral oils, and distillation products increased sharply from $1.7 billion in 2024 to $4.4 billion in 2025, representing a substantial rise of approximately 158.8%. This surge explains a significant portion of the increase in American exports to Egypt and the widening of the American trade surplus. Imports of oilseeds, oleaginous fruits, and various grains also rose from $1 billion to $1.7 billion, marking a 70% increase.

By contrast, imports of organic chemicals from the United States declined from $640 million to $550 million, reflecting a decrease of 14.1%, while imports of machinery and mechanical appliances remained broadly stable at approximately $440 million with little notable change. Imports of pharmaceutical products also recorded a slight increase, rising from $280 million to $290 million, or 3.6%.

Second: Egypt in the 2026 Reports of the US Administration

The reports issued by the United States reflect Washington’s assessment of Egypt’s economic and trade environment. In the Special 301 Report concerning the protection of intellectual property rights, the US administration maintained Egypt on the “Watch List,” despite acknowledging several positive measures undertaken by Egypt to strengthen intellectual property protection. At the same time, the report noted that Egyptian customs authorities still lack ex officio authority to suspend the release of goods suspected of violating intellectual property rights, while judicial procedures remain slow and deterrent enforcement measures insufficient.

Meanwhile, the Foreign Trade Barriers Report 2026 emphasized that Egypt continues to maintain a relatively high tariff structure, particularly in the agricultural sector, and that Washington still considers certain Egyptian tariff rates excessively high and restrictive to market access.

How Could These Reports Pose Challenges to Egyptian Trade Policy?

The primary challenge stems from the negative signals such reports—particularly the Special 301 Report—may convey to investors and foreign companies regarding the level of protection and enforcement of intellectual property rights within the Egyptian market, especially in sectors dependent on technology, pharmaceuticals, and creative industries. This could ultimately influence foreign investment decisions and shape the orientation of multinational corporations toward the Egyptian market in comparison with competing markets.

As for the Foreign Trade Barriers Report, it represents a comprehensive instrument through which Washington identifies what it considers “barriers” to trade. The issues raised in the report generally constitute the core agenda of the American side during negotiations with Egypt within the framework of the periodic meetings of the Trade and Investment Framework Agreement Council (TIFA).

Fifth: Strategic Implications of American Trade Policy and International Responses

For the International Trading System:

- The ongoing transformations in international trade policy do not merely reflect temporary changes in tariff levels or patterns of trade agreements, but rather point to a broader structural transformation in the nature of the global trading system itself.

- International trade is no longer confined to considerations of market access alone; it has become increasingly linked to issues such as economic security, supply chain resilience, and the redistribution of production centers. Consequently, the traditional model based on open globalization is gradually giving way to a more selective and flexible framework.

- The ruling of the Supreme Court of the United States concerning tariffs was not the direct cause behind the emergence of the new wave of trade agreements, but rather acted as an accelerating factor for trends that were already underway. It reinforced states’ awareness of the need to diversify partnerships and reduce dependence on specific economic centers.

- American actions have demonstrated that trade policy instruments have become increasingly complex and more closely tied to industrial and strategic objectives, extending far beyond the traditional concept of trade protectionism.

- Emerging economies now face the challenge of securing a position within the new international trading system, whether to preserve their current standing or mitigate the repercussions of the evolving arrangements being concluded among the major actors within the global trade architecture. These developments will inevitably affect the position of emerging economies within supply chains, trade routes, and investment destinations.

For Egypt:

- These transformations may impose growing challenges related to the erosion of certain traditional preferential advantages, intensifying competition in key export markets, and increasing pressures associated with environmental, regulatory, and digital standards.

- At the same time, however, these shifts also create potential opportunities for Egypt to strengthen its position within regional and international supply chains, particularly in the fields of energy, logistics, and industries linked to the green transition.

- Such opportunities depend not only on Egypt’s geographic location or its existing trade agreements, but fundamentally on its ability to develop a more competitive production base, deepen integration into global value chains, and formulate a more flexible trade and industrial policy capable of responding to the rapid transformations taking place within the global economy.

- These transformations also provide Egypt with opportunities to reinforce its strategic position within international trade routes and investment destinations, thereby strengthening its role within the global trade and investment landscape.

In conclusion, it can be argued that American trade policy has reinforced the conviction among states that the global trading system has become more volatile and less predictable. This has driven countries to accelerate efforts toward trade diversification, supply chain security, and deeper regional integration. What is currently unfolding is not merely a direct reaction, but rather an expression of a transitional phase in the structure of the international trading system—one that presents significant challenges for emerging economies while simultaneously reflecting the rise of more pluralistic and flexible patterns in international economic relations.