As the world was turning the corner after a period of lockdown and economic crises due to Covid-19 that caused world economies to stagnate, the Russo-Ukrainian war brought about a spate of crises at the political and economic levels. Direct impacts of the war include rising inflation, declining growth, disruption of supply chains due to scarcity and higher cost of raw materials, commodities, energy, and transportation. Inflation is likely to continue to rise, with the average inflation rate expected to rise in 12 months.

In effect, the Russo-Ukrainian conflict represents a major blow to the global economy, as it harms growth and raises prices. The FAO Food Price Index (FFPI), which tracks monthly changes in the international prices of a basket of commonly traded food commodities, increased by 12.6 percent between February and March, hitting its highest level since it was introduced in 1990. Additionally, the FAO Cereal Price Index jumped by a greater rate (17.9 percent during this period), reflecting higher global prices of wheat and coarse grains, largely due to disruption of exports from Russia and Ukraine, two of the world’s major wheat exporters.

The Ukraine war will have a considerable bearing on three main aspects. First, the high prices of basic commodities such as food and energy will further push up inflation, eroding the value of income and affecting demand. Second, neighboring economies, in particular, will also suffer disruption of trade, supply chains, and remittances, and there will be a historically high refugee flow. Third, lower business confidence and increased investor uncertainty will affect asset prices, bringing about tighter financial conditions and possibly stimulating capital outflows from emerging markets.

Russia and Ukraine are significant producers of basic commodities, and the disruption in commodity markets gave rise to hikes in food as well as oil and natural gas prices. In effect, Russia and Ukraine account for 30 percent of global exports, and sharp increases in food and fuel prices could raise the risk of unrest in some regions, from sub-Saharan Africa and Latin America to the Caucasus and Central Asia. Further, food insecurity is likely to increase in parts of Africa and the Middle East.

In the long term, the war could fundamentally change the global economic order if energy trade is shifted, supply chains are reconfigured, payment networks are fragmented, and reserve currency holdings reconsidered. The rising geopolitical tension increases the risks of economic disintegration, especially for trade and technology, and Russia’s invasion of Ukraine has resulted in an increase in oil prices –which were already high due to pent-up consumer demand following Covid-19– to more than $110 a barrel, as many Western countries imposed severe sanctions against Russia in retaliation.

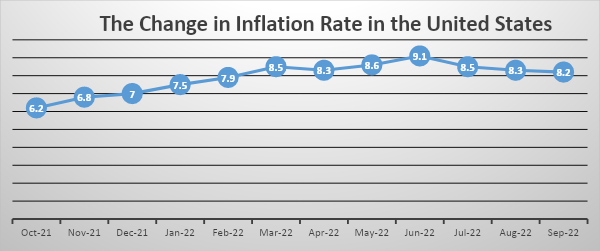

Inflation in the US

Annual US inflation rate slowed for the third consecutive month to 8.2 percent in September 2022, the lowest rate in seven months, down from 8.3 percent in August. It remains, however, above market expectations of 8.1 percent. The energy index rose by 19.8 percent, below 23.8 percent in August, due to the price hikes of gasoline (18.2 percent vs. 25.6 percent), fuel oil (58.1 percent vs. 68.8 percent) and electricity (15.5 percent vs. 15.8 percent, the highest since 1981). A slight slowdown in the cost of food (11.2 percent vs. 11.4 percent, the highest since 1979) and second-hand cars and trucks (7.2 percent vs. 7.8 percent) have been observed. Home prices rose faster as well (6.6 percent vs 6.2 percent). Meanwhile, inflation base rate, excluding volatile food and energy prices, rose to 6.6 percent, i.e. the highest since August 1982, above market expectations of 6.5 percent, signaling the continued inflationary pressures.

Figure 1: The change in inflation rate in the United States

Inflation in Europe

Real economic growth in the European Union (EU) is now expected to fall below 3 percent in 2022, down from 4 percent estimated by the European Commission before the war. More trade disruptions and the growing economic sanctions could push the European economy into recession, and the war in Ukraine threatens to undermine Europe’s economic recovery. The Russian invasion of Ukraine caused a massive humanitarian crisis, with nearly seven million Ukrainians fleeing the country. The conflict in Ukraine and the arising sanctions have also disrupted exports of commodities such as minerals, food, oil and gas from the region, pushing inflation to its highest level in decades. Perhaps the slowing growth is particularly evident in countries neighboring Ukraine, such as Poland and Hungary, which host large numbers of Ukrainian refugees. Italy and Germany, which rely heavily on Russian oil and gas, are also feeling the pressure.

Noticeably, optimism has slipped in the Eurozone more than in non-European countries. In the Eurozone, Chief Financial Officer (CFOs) are most pessimistic about business confidence in Spain (66 percent), Austria (61 percent), Greece (53 percent), and Germany (52 percent). UK CFOs (47 percent), are, however, the most pessimistic about business confidence.

The losses in Ukraine are tremendous. The unprecedented sanctions against Russia will impair financial intermediation and trade, inevitably leading to a deep recession. The depreciation of the ruble will increase inflation, which will give rise to a further decrease in the living standards of the population. Energy is the main indirect channel to Europe, as Russia is an important source of natural gas to the old continent. These repercussions will increase inflation and slow the recovery from the pandemic. Financing costs and refugee numbers are likely to increase in Eastern Europe. European governments may also come under financial pressures due to additional spending on energy security and defense budgets. While foreign exposures to plunging Russian assets are modest by global standards, pressures on emerging markets may grow should investors seek safer havens.

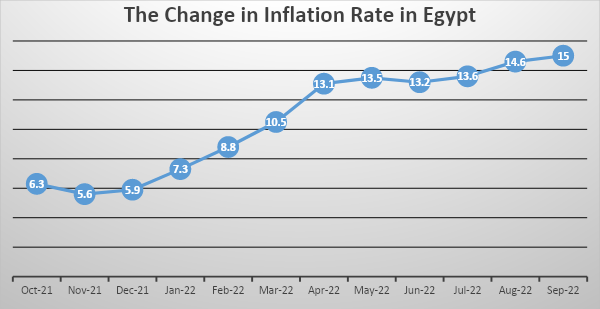

Inflation in Egypt

The annual inflation rate in urban areas in Egypt increased to 15 percent in September 2022, up from 14.6 percent in August 2022. This is driven by the rise in the prices of non-food commodities, i.e. the main reason that continues to be affecting inflation rates since May 2022. The rise of urban inflation in September 2022 was driven by the rise in basic commodity prices due to the rise in the prices of basic food commodities, consumer goods, and services. The rise in the set prices of defined commodities and services was mainly reflected in the rise of prices of cigarettes and subsidized rice.

Figure 2: The change in inflation rate in Egypt

The increase in the annual urban inflation in September 2022 can be attributed to the increase in the annual contribution of non-food commodities, where the annual rate of inflation of non-food commodities increased for the eleventh month in a row, recording 12 percent in September 2022, from 10.8 percent in August, i.e. the highest rate since May 2019, whereas the annual food inflation rate decreased to 21.7 percent in September 2022, from 23.1 percent in August 2022.