Russia and Ukraine are among the most significant producers of agricultural commodities in the world and they make a major contribution to the total production of the grain sector. Both countries are net exporters of agricultural products and play leading roles in supplying global markets with food commodities, particularly barley, wheat, and corn.

However, the disruptions caused by the Ukraine war exposed global food markets to several risks, including the inability to meet the demand for imports and the rise in food prices internationally, which pushed the importing countries to look for alternative sources (e.g. India and Argentina) to meet their needs of food commodities and grains, especially wheat.

Changes in Russian and Ukrainian Wheat Production and Exports

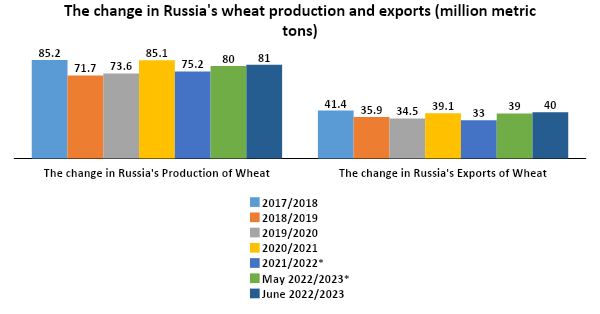

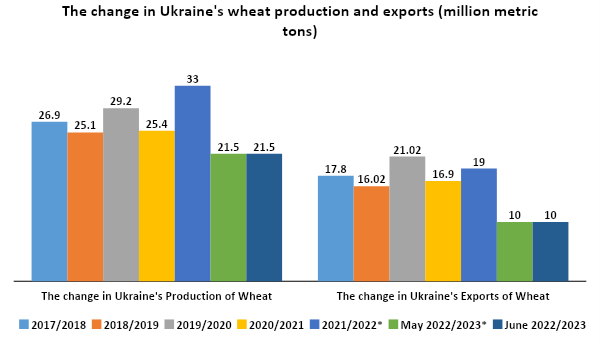

In 2020/2021, Russia was ranked the third largest wheat producer in the world behind China and India, with a total production of about 85 million metric tons whereas Ukraine was ranked eighth with a production of about 25 million metric tons. However, a look at exports, we find that Russia’s exports of wheat accounted for 17.6 percent of the total global wheat exports, leading Russia to become at the forefront of wheat exporting countries, with exports amounting to about 39 million metric tons ($7.9 billion). Ukraine exported 16.9 million metric tons valued at $3.6 billion, according to the US Department of Agriculture.

With respect to the two countries’ production and exports of wheat during 2021/2022, Russia’s wheat production is expected to decline to about 75 million metric tons whereas Ukraine’s production is expected to rise despite the war to record 33 million metric tons. Russia’s exports of wheat will also decline to reach 33 million metric tons but Ukraine’s exports will increase to 19 million metric tons. The following figures show the change in Russia’s and Ukraine wheat production and exports.

Figure 1: The change in Russia’s wheat production and exports, 2017/2018 – June 2022/2023

Figure 2: The change in Ukraine’s wheat production and exports, 2017/2018 – June 2022/2023

The harvest of winter wheat was set to start in early July in Ukraine, but due to the war, 20-30 percent of the areas where winter crops are grown will remain unharvested during the 2022/2023 season and the availability of fuel will determine the amount of acreage to be harvested and the yield crops to be stored.

Overall, more than 30 net importers of wheat depend on the two countries for more than 30 percent of their wheat needs. For example, Eritrea procured almost all of its wheat imports in 2021 from both Russia (53 percent) and Ukraine (47 percent).

Alternative Wheat Producing and Exporting Countries

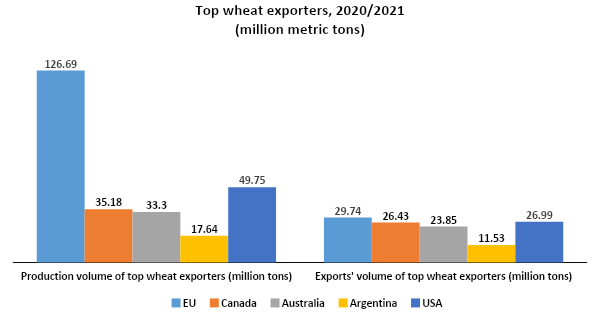

China and India are among the leading wheat-producing countries globally, with their production accounting for 17.3 and 13.9 percent of the global wheat production, respectively in 2020/2021. China’s wheat production amounts to 134.25 million tons whereas that of India amounts to 107.86 million tons. However, both countries contribute a small share of the total wheat exports (China: 0.45 percent and India: 1.3 percent), i.e. 0.76 and 2.56 million tons, respectively. In May, India announced imposing a ban on wheat exports after climate change severely affected the wheat yield. While India is not a major exporter of wheat, its ban brought about instability in global markets, with Benchmark wheat futures in Chicago rising nearly by 6 percent. The following figure shows wheat production and exports of countries other than Russia and Ukraine.

Figure 3: Top wheat exporters, 2020/2021

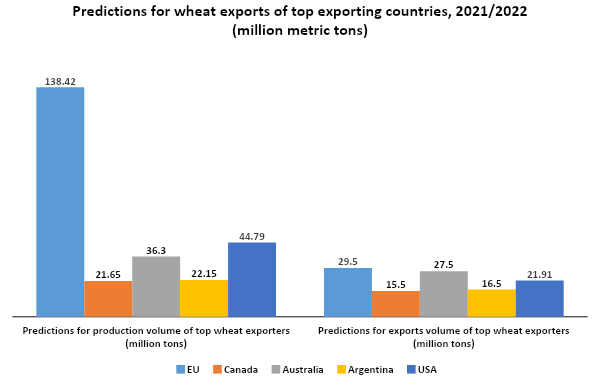

According to data from the US Department of Agriculture, there are expectations of an increase in the quantities produced and exported of wheat in Argentina, Australia, and the European Union whereas Canada’s production and exports of wheat are projected to decline by 61.5 percent in 2021/2022 relative to 2020/2021. However, the cultivated area of wheat in Canada is expected to increase to a maximum, causing production to return to the normal levels and hence exports will likely increase, according to the forecasts of Statistics Canada for 2022/2023. Likewise, the United States’ production and exports of wheat will decrease in 2021/2022 for considerations related to the returns of wheat, the changes in government programs that give farmers more flexibility in rotation planning. The following figure presents predictions for wheat exports of top exporting countries in 2021/2022.

Figure 4: Predictions for wheat exports of top exporting countries, 2021/2022

The Global Impact of the Ukraine War on Wheat Production and Exports

The outset of the war greatly undermined Ukraine’s grain exports, due to the lack of access to the Black Sea ports and the limited alternative means of transportation, e.g. rail, river, or road transportation, to make up for the lack of seaborne shipments. FAO’s initial projections for 2022/2023 (June and July) indicate that Ukrainian wheat exports could drop by 50 percent (i.e. 9 million tons) relative to the year 2021/2022. If this happens, the expected decline in Ukrainian shipments and the disruptions to production in alternative sources from Australia and Argentina could outpace the expected shipments from the European Union, Canada, and Russia, bringing about a contraction in global wheat trade compared to the 2021/2022 levels.

Most of the countries that normally import from Ukraine are expected to find other alternatives that help maintain their total imports close to last season’s levels. For example, wheat imports of Egypt (the largest global importer of wheat) are expected to slightly increase in 2022/2023, given the government measures aimed at facilitating imports from other countries, such as Argentina and India.

As for Iran (the fifth largest importer of wheat in the world in 2021/2022), which imported on average more than 60 percent of its wheat imports from Ukraine and Russia during 2016/2017 – 2020/2021, its wheat imports are expected to decrease by 57 percent on a year-to-year basis in 2022/2023.

The Global Outlook of the US Department of Agriculture for wheat in 2022-2023 indicates that there would be a decline in supplies, a decrease in consumption, a partial decline in wheat trade, and a slight decrease in the final stockpile. Global market supplies of wheat also fell by 1.7 million tons, reaching 1052.8 million tons. The increase in Russia’s wheat production will offset the decline in wheat supplies from India, which fell by 2.5 million tons, recording 106.0 million tons, where extreme temperatures in March and April led to lower yields. The Indian government also worked on imposing a ban on exports to some destinations to ensure adequate domestic supplies.

World trade of wheat is expected to decline in 2022/2023 by 0.3 million tons, reaching 204.6 million tons, as the decline in exports from India has not been fully offset by increased exports from Russia and Uzbekistan.

Russia’s production has been stepped up by one million tons, recording 81 million tons given the increase in winter wheat under favorable weather conditions. Similarly, Russia’s exports increased by one million tons, reaching 40 million, leading Russia to become the second largest exports ever. Russian wheat supplies are projected to rise in 2022/2023, as its export prices are more competitive than most other exporters. Global stockpiles for 2022/2023 are projected to be reduced by 0.2 million tons, recording 266.9 million, i.e. the lowest level in six years.

Global consumption in 2022/2023 is expected to decline by 1.5 million tons, recording 786 million, given the low feedstocks, India’s consumption of the residual wheat, and the reduced use of grain and seed for industrial use in Sri Lanka and Argentina.

While wheat production and exports of major exporting countries are expected to increase (except those of Ukraine and Canada) the Russo-Ukrainian war will affect the wheat markets and prices which would pose a challenge to wheat-importing countries, particularly Middle Eastern and North African countries, where the war threatens to push prices of foodstuffs up, particularly with the decreasing cultivated area of wheat in Ukraine under the Russian blockade, and the blockade of large quantities of wheat in the Black Sea ports, a situation that prompted wheat-importing countries to make efforts to get wheat from alternatives countries such as France and Germany or from countries such as Kazakhstan, Argentina, Canada, and Australia.